Reserve Diversification: Gold, Not Renminbi

The dollar's reserve share actually rose last quarter. The real story in the data is gold, not the currency popularly assumed to be the dollar's challenger

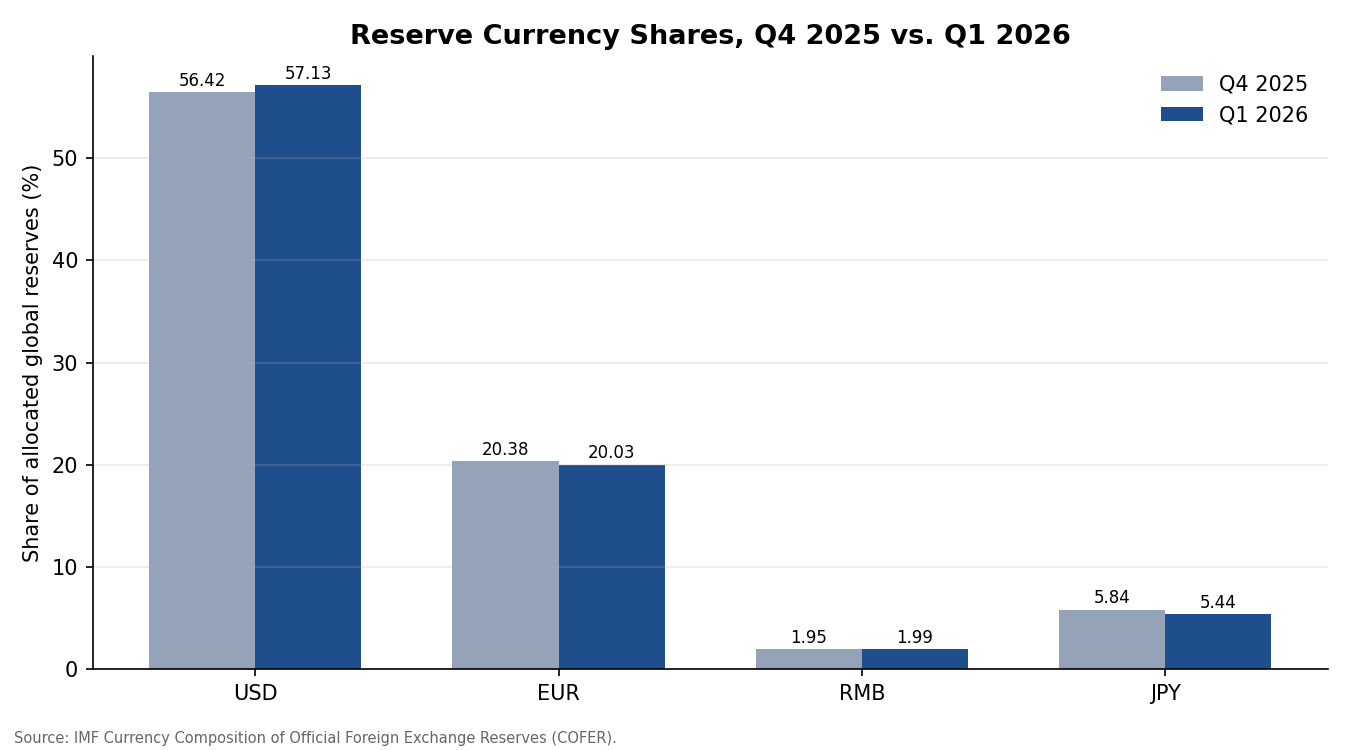

The most recent IMF data complicates the 'de-dollarization' narrative rather than confirming it. In the first quarter of 2026, the US dollar's share of allocated global reserves rose to 57.13%, up from a revised 56.42% in the fourth quarter of 2025 -- driven roughly half by the dollar's own appreciation against major currencies, a valuation effect rather than a change in how central banks are allocating new reserves. The euro's share fell slightly to 20.03%. The presumed principal challenger, the Chinese renminbi, inched up to just 1.99% -- still, after more than a decade of predictions to the contrary, essentially negligible as a reserve currency. The real story in the data is gold. In 2025, gold's value in official reserve portfolios surpassed US Treasuries for the first time -- but the IMF itself attributes that shift almost entirely to gold's price appreciation, not to a surge in central bank buying.

Evidence Base

This piece draws on the IMF's Currency Composition of Official Foreign Exchange Reserves (COFER) data, published quarterly with roughly a three-month lag, most recently for Q1 2026. COFER is sourced externally rather than from this platform's canonical data layer -- disclosed explicitly, consistent with how Institutional Strategy essays are distinguished from data-driven Deep Dives elsewhere on this platform. This piece uses more recent data (Q1 2026) than this platform's own flagship research papers, which were written against Q4 2025 figures -- the Q1 2026 update meaningfully changes the picture those papers described, and this piece corrects that rather than repeating the earlier framing uncritically.

Reserve Currency Shares, Q4 2025 vs. Q1 2026

Reading the Data Correctly

The single most important analytical distinction in this piece is between a valuation effect and an allocation decision. When the dollar appreciates against other reserve currencies, existing non-dollar holdings become worth fewer dollars, which mechanically raises the dollar's share of total reserves -- without any central bank actually buying more dollars. The IMF's own commentary attributes roughly half of Q1 2026's dollar-share increase to exactly this mechanism. The same logic applies to gold's overtake of Treasuries: a rising gold price increases the dollar value of existing gold holdings without requiring a single additional ounce to be purchased.

Read this way, the accurate structural claim is narrower and more defensible than 'de-dollarization': central banks have been genuinely, gradually diversifying reserve purchases toward gold for several years running, a real allocation trend independent of price -- but this has not translated into a growing role for any rival currency, least of all the renminbi, and the dollar's headline reserve share remains volatile quarter to quarter based on exchange-rate movements that have nothing to do with diversification at all.

What Could Be Wrong

This piece cannot cleanly separate, within the gold data specifically, how much of 2025's reserve-share shift was valuation versus actual net purchasing. A single quarter's dollar-share increase is not, on its own, proof that the longer gradual decline documented since 2000 has reversed -- one quarter of data cannot resolve a multi-decade question either way.

Implications

The evidence supports a specific, narrower positioning implication than the popular narrative: investors and allocators tracking 'de-dollarization' as a renminbi-ascendance story are tracking a trend the data does not support -- the renminbi's reserve role has been flat for years. The trend the data does support is a genuine, gradual, price-independent shift in central bank gold purchasing, which is a different investment thesis (a case for gold specifically) than a case for any specific alternative reserve currency.

Monitoring Points

Next COFER release, due with the standard three-month lag -- whether Q1 2026's dollar-share increase persists or reverses in Q2 is the most immediate open question this piece leaves unresolved. Central bank gold purchase volumes, tracked independent of price, pending data that separates volume from valuation more precisely than COFER's headline share figures allow.