Global Liquidity Monitor: Launch Edition

US dollar liquidity has accelerated in 2026, coinciding with the Fed's shift from tightening to balance-sheet stabilization -- the first installment of an ongoing monitor, honestly scoped to what the platform's data supports today

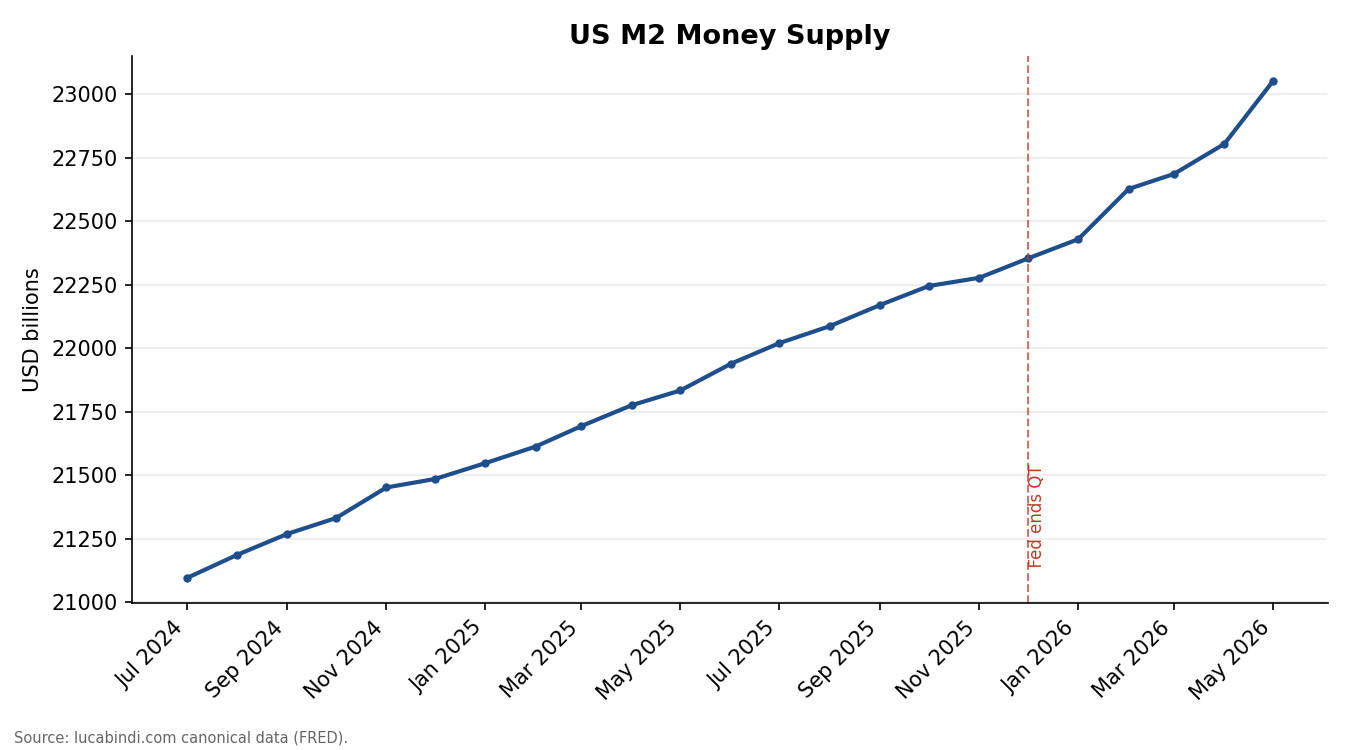

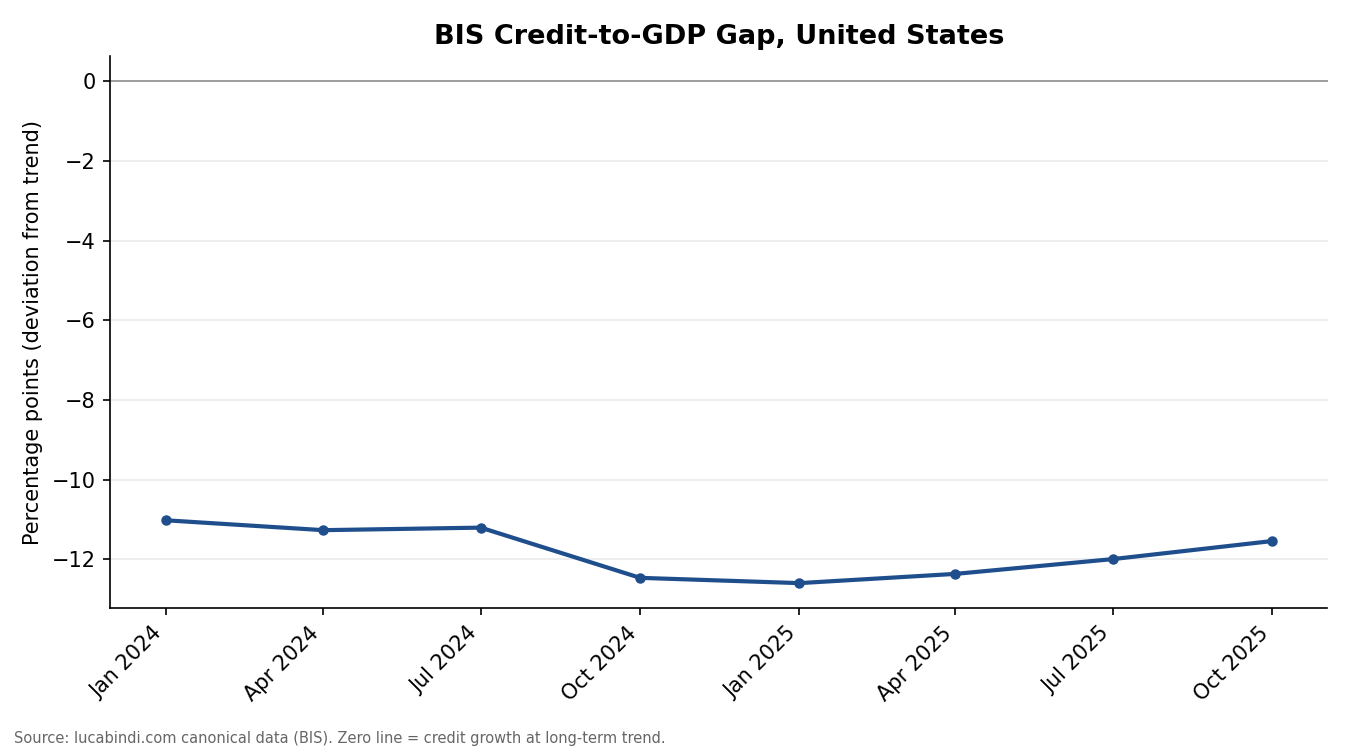

This is the first installment of an ongoing Global Liquidity Monitor. It is launched under that name deliberately, but scoped honestly: the platform's current data supports a genuine US dollar liquidity read, not yet a truly global one. Two distinct signals are worth tracking together. First, US M2 money supply has clearly accelerated through the first five months of 2026, after a full year of steadier growth -- a shift that coincides directly with the Federal Reserve's December 2025 decision to end quantitative tightening and begin stabilizing its balance sheet around an 'ample reserves' level. Second, the BIS credit-to-GDP gap has been gradually narrowing throughout 2025, moving from -12.59 percentage points in January to -11.54 in October, meaning credit growth has been slowly closing the gap with trend growth even while remaining below it. Neither signal alone would be conclusive; read together, they describe a liquidity environment that is genuinely loosening, gradually, from a below-trend starting point.

Evidence Base

M2 data is drawn from the Federal Reserve via FRED, monthly, single-sourced. The BIS credit-to-GDP gap is drawn directly from the Bank for International Settlements' own published series via the platform's canonical data, quarterly, with a reporting lag reflected in the October 2025 reading being the most recent available as of this writing.

US M2 Money Supply

Reading the Two Signals Together

Money supply and credit growth measure genuinely different things -- M2 reflects the stock of money in the economy, while the credit-to-GDP gap reflects the pace of credit expansion relative to trend -- and it would overstate the evidence to claim they mechanically drive one another. What can be said directly from the data: both are currently moving in the same direction, and the M2 acceleration's timing lines up with a specific, identifiable policy event (the Fed's own December 2025 framework shift) rather than appearing as an unexplained trend break.

BIS Credit-to-GDP Gap, United States

What Could Be Wrong

This edition's biggest limitation is scope, not method: two US-only series cannot support a genuinely 'global' liquidity read, and this piece does not claim to provide one. Within the US-only scope, the M2/QT-timing connection is a coincidence in timing that this piece finds genuinely suggestive, not a causal claim the current evidence proves.

Implications

The evidence here supports monitoring, not a directional call: a liquidity environment moving from tight toward looser, gradually, is relevant context for credit and asset-price conditions generally, but two data points on their own don't yet justify a specific positioning recommendation. The clearest implication is that this combination of indicators is worth tracking as a standing pair going forward, which is the actual purpose of launching this as a named, recurring monitor rather than a single Deep Dive.

Monitoring Points

M2 growth pace, ongoing -- specifically whether the 2026 acceleration continues, stabilizes, or reverses. BIS credit-to-GDP gap, next reading, due on its standard quarterly cadence. Monitor scope expansion to additional central banks and genuine cross-border liquidity measures, tracked explicitly as a stated goal for future editions.